In the volatile theater of 2026, a sudden shift in the semiconductor market has sent a chill through the boardrooms of Silicon Valley. For nearly two years, the narrative was one of scarcity: a brutal RAM shortage that saw memory prices surge by over 200% year-on-year, driven by the voracious appetite of Generative AI. But last week, the trend snapped. RAM prices have begun a sharp, unexpected descent.

To the casual observer, cheaper memory looks like a win for innovation. But to those monitoring the heartbeat of the cloud, this price drop is a symptom of a deeper malaise. Across the globe, massive AI and Cloud infrastructure projects—once hailed as the “space race” of our decade—are hitting the brakes. Nearly half of all U.S. data center projects planned for 2026 are now facing delays or total cancellation.

The “Memory Mirage” is the illusion that the AI boom is cooling. In reality, the industry has hit a wall of its own making. This post dissects the structural fractures causing this stall, from the electrical grid’s breaking point to the “Demand Fatigue” that has finally reached the hyperscalers. If 2025 was the year of “Digital Rust,” 2026 is the year of the Infrastructure Hangover.

1. The Bullwhip Effect: From Scarcity to Surplus

To understand the necessity of modern architectural pipelines, we must first address the systemic The semiconductor industry has always been a victim of the “Bullwhip Effect”—where small fluctuations in demand at the retail level cause massive swings in manufacturing supply. Between 2024 and early 2026, manufacturers like Samsung and SK Hynix pivoted almost their entire capacity toward High Bandwidth Memory (HBM), the specialized fuel for AI accelerators like NVIDIA’s Blackwell.

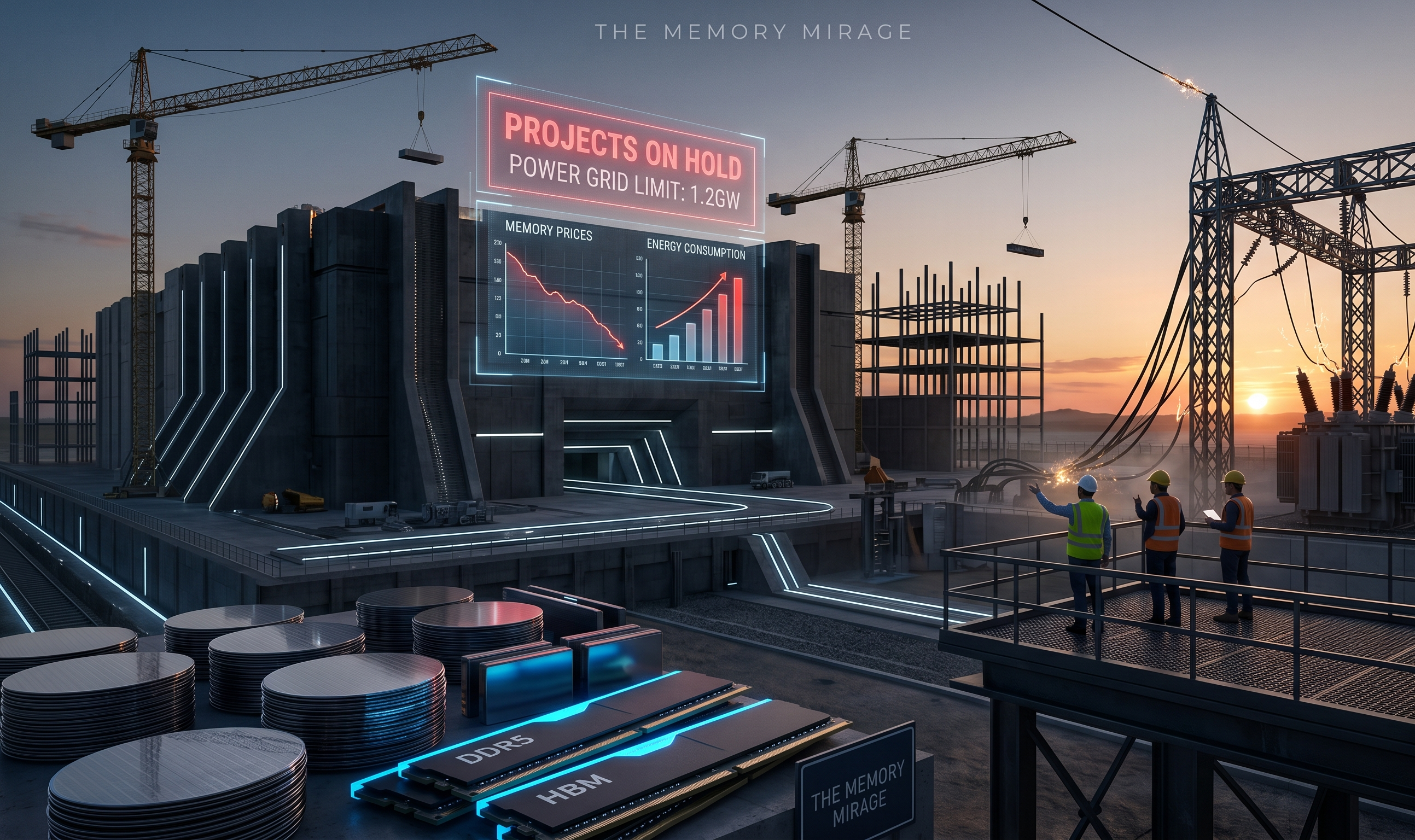

However, as of March 2026, we are seeing the first major market correction. According to reports from TechBehemoths, the “RAMmageddon” price peak has finally broken. This isn’t because we have enough memory; it’s because the projects that were supposed to consume that memory are stuck in limbo. When a $5 billion data center project is delayed by 18 months due to a lack of power transformers, the RAM orders for that project are canceled or deferred. This creates a sudden “phantom surplus,” forcing prices down even while the long-term structural need remains unmet.

2. The 1.2-Gigawatt Wall: Why the Grid is Saying “No”

The primary reason for the infrastructure stall isn’t silicon—it’s copper and electricity. While the tech world focused on chip architecture, the physical world ran out of power. Recent data indicates that only one-third of data centers expected to deliver new capacity in 2026 are actually under construction.

The bottleneck is two-fold. First, the delivery times for high-voltage transformers have stretched from two years to nearly five. You can buy 100,000 GPUs tomorrow, but if you cannot hook them to the grid, they are high-tech paperweights. Second, the cost of these components has doubled, largely due to a heavy reliance on specialized electrical parts from overseas that are now subject to tightening trade restrictions. The result? Hyperscalers like Microsoft and Google are “holding” projects because they simply cannot flip the switch.

3. “Demand Fatigue” and the C-Suite Reality Check

For eighteen months, “AI” was a magic word that justified any expenditure. But as we move deeper into 2026, the “AI ROI gap” is widening. Investors are starting to ask: Where is the revenue? Many companies that announced massive data center expansions in 2024 are now utilizing what analysts call “Supply Chain Excuses” to mask a strategic retreat. As noted by industry insiders on platforms like Reddit’s technology circles, firms that promised three data centers to appease stockholders are quietly scaling back to one. This “Demand Fatigue” among enterprise buyers has cooled the spot market for RAM, contributing to the price drop. Companies are no longer hoarding memory at any cost; they are waiting to see if their AI agents actually move the needle on the bottom line.

4. The Ghost of 2018: Is History Repeating Itself?

This isn’t the first time the memory market has cratered after a hype cycle. We saw a similar “boom-bust” in 2018 when the initial surge of cloud migration and the first crypto-mining craze led to a massive overproduction of DRAM. When the crypto bubble popped and cloud growth stabilized, RAM prices plummeted by nearly 50% in a single year.

The current drop feels eerily familiar, but with a twist. In 2018, the surplus was in standard DDR4. Today, the price drop is hitting standard server RAM (DDR5) because manufacturers over-compensated for the AI boom. However, the specialized HBM3e memory remains in a “permanent shortage.” This creates a bifurcated market: while consumer PCs and legacy servers get cheaper to build, the cutting-edge AI clusters remain prohibitively expensive, further stalling projects that can’t afford the “premium” silicon.

5. The “18-Month Rule” and the Cost of Inaction

In our previous discussion of the “18-Day Rule” for cloud-native expansion, we highlighted the speed of the cloud. But in 2026, we are facing the 18-Month Rule of Infrastructure. If a project isn’t already “ground-broken” and “power-secured,” it is effectively dead until 2028.

The fall in RAM prices provides a temporary window of opportunity for “Lean AI” startups. While the giants are stalled by massive grid-scale problems, smaller, more efficient players can now snag high-performance memory at a discount to build localized, edge-computing solutions. The companies “holding” are the ones trying to build the ocean; those building the streams are finding that the lower component costs are finally making their smaller-scale projects viable.

6. Geopolitical Friction: The Chinese Component Crisis

A critical factor in the stalling of Western AI projects is the “invisible supply chain.” Over half of the electrical components required for U.S. data centers—specifically batteries and switchgear—are currently sourced from manufacturers in Asia.

As trade tensions escalate in early 2026, these supply lines have frayed. It is a paradox of modern tech: the world’s most advanced AI models are being held back by a shortage of mid-20th-century electrical hardware. The fall in RAM prices is, in part, a reflection of the market realizing that the “Compute” (RAM/GPUs) is ready, but the “Housing” (Data Centers) is locked behind a geopolitical stalemate.

7. Efficiency Gains: The Google Effect

Innovation is also a “silent killer” of demand. In late 2025 and early 2026, major breakthroughs in Memory Efficiency were announced. Google, for instance, implemented new algorithmic optimizations that allowed their LLMs to run with 30% less DRAM overhead.

When the world’s largest consumer of RAM suddenly finds a way to use 30% less of it, the market reacts instantly. This “Efficiency Correction” is a healthy part of the tech cycle, but it contributes to the perception of a falling market. Companies are realizing they don’t need to “brute force” their way through AI infrastructure; they can “optimize” through it. This shift from quantity to quality is a primary driver of why companies are holding off on massive hardware buys.

8. The Environmental Pivot: ESG vs. Expansion

In 2026, the “Green Tax” has become a boardroom priority. The massive energy consumption of stalled AI projects has drawn the ire of regulators. Many cloud providers are pausing projects not because they lack the money, but because they cannot meet the new Net-Zero mandates for 2027.

The fall in RAM prices is a byproduct of this pause. As companies wait for Small Modular Reactors (SMRs) or geothermal power solutions to come online, their hardware procurement is on ice. The “Cloud-First” strategy of 2025 is now being replaced by a “Green-First” strategy. If you can’t power it cleanly, you can’t build it—regardless of how cheap the RAM is.

Conclusion: The Survival of the Optimized

The falling RAM prices of 2026 are not a sign of AI’s death, but of its Industrial Maturation. The “gold rush” phase, where companies bought everything in sight, has ended. We have entered the “Settlement” phase, where logistics, power, and efficiency dictate who wins.

The companies “holding” their projects are those that failed to account for the physical realities of the grid. Those who will thrive are the ones using this price dip to refactor their code, optimize their memory usage, and prepare for a more surgical, efficient expansion. The “Digital Rust” is still eating the old world, but the new world is learning that even the cloud needs a solid, powered foundation to stand on.

References:

- IDC, Dec 18, 2025, “Global Memory Shortage Crisis: Market Analysis and the Potential Impact on 2026.” https://www.idc.com/resource-center/blog/global-memory-shortage-crisis-2026/

- TechBehemoths, March 31, 2026, “RAM Crisis: How the Shortage and Sudden Drop Affects IT Companies.” https://techbehemoths.com/blog/ram-crisis-shortage-affects-businesses

- The AI Innovator, April 9, 2026, “AI Data Center Buildout to Slow Due to Equipment Shortages.” https://theaiinnovator.com/ai-data-center-buildout-slowdown/

- Bloomberg News, April 1, 2026, “America’s AI Build-Out Hinges on Chinese Electrical Parts.” https://www.bloomberg.com/news/features/2026-04-01/us-ai-data-center-expansion/

- Sportskeeda Tech, March 29, 2026, “What really caused the global RAM price surge and sudden drop?” https://tech.sportskeeda.com/laptops/what-really-caused-global-ram-price-drop

- Wikipedia, 2026, “2024–present global memory supply shortage (The RAMmageddon).” https://en.wikipedia.org/wiki/2024–present_global_memory_supply_shortage

- LCMH, Feb 10, 2026, “2026 RAM Shortage: Why Your Servers Will Cost More.” https://lcmh.fr/en/articles/2026/ram-shortage-2026-cloud-solution/

- Tom’s Hardware, April 10, 2026, “Half of planned US data center builds have been delayed or canceled.” https://www.tomshardware.com/tech-industry/artificial-intelligence/data-center-delays-2026

Leave a Reply